U.S. venture capital deal value reached about $340 billion in 2025, short of the 2021 peak of nearly $360 billion. Sub-$100 million deal count hit a at least a 10-year low. Venture debt set its own record of over $60 billion deployed, however, deal volume has been decreasing.

A narrow set of companies, geographies, and sectors seem to be capturing most of the absolute dollars. A large cohort of companies sits between the extremes.

These are businesses with resilient revenue, improving capital-efficiency, and strong management teams with a plan, but lack the narrative, AI angle, or certain defensibility that attracts premium equity pricing today. Many raised in 2021 or 2022, kept building, and now face a market pricing them on different terms.

We call them the missing middle: companies who are still growing, but have financing needs that differ from what the concentrated and at times complacent market today looks for.

The market has bifurcated: for these companies, the struggle will be to find the right capital fit: how to blend equity, debt, or hybrid capital.

In 2025, U.S. VC deal value reached approx. $340 billion across just over 16,700 transactions, but deal count has not recovered.

The PitchBook 2025 Annual Valuations Report showed the concentration: half of all venture dollars went into <1% of completed deals. The top 10 companies held >40% of the value. PitchBook also estimated that 222 of 857 tracked unicorns may have slipped back below $1 billion in value, a reminder that headline strength hides extensive repricing underneath.

On the fundraising side, U.S. firms raised around $66 billion across about 540 funds in 2025, the lowest annual total in more than a decade. Andreessen Horowitz’s $15 billion January 2026 raise alone equalled more than 18% of all VC commitments. Capital is concentrating into fewer, larger vehicles that pursue fewer, larger positions. There is a growing seed and growth equity movement that plans to fund companies with more patient capital, for longer. However, in absolute dollars, these new and growing entrants are still being dwarfed.

The market, which is concentrating at the top, only reopened for a narrow set of companies. For many others, access remains constrained. The fit they need is harder to find.

Split the data by deal size and the concentration turns structural.

For transactions under $100 million, quarterly deal count fell to 1,346 in Q4 2025, a 69% drop from the Q1 2022 peak and the lowest level in 12 years.

Above $100 million, the opposite happened. Large transactions climbed from early 2023 onward. In Q4 2025, 117 deals above $100 million totalled $56 billion.

The venture market now behaves like two different markets sharing the same headline numbers.

At the top, a small number of AI and AI-adjacent companies command unprecedented capital: mega-rounds, billion-dollar valuations, and fierce competition among the largest funds for allocations. This market is loud, visible, and well-served.

At the bottom, some early-stage and AI-native companies can raise smaller rounds, use AI-assisted tools to move faster, and in some cases delay or skip later financings. This varies, but it reduces equity demand for part of the pipeline.

In the middle sits the cohort we and our trusted partners want to see succeed: the operators with $3 million to $20 million of revenue, 20% to 60% growth, and unique financing needs that require fit over all else.

Three forces help explain the disappearance of sub-$100 million deal flow.

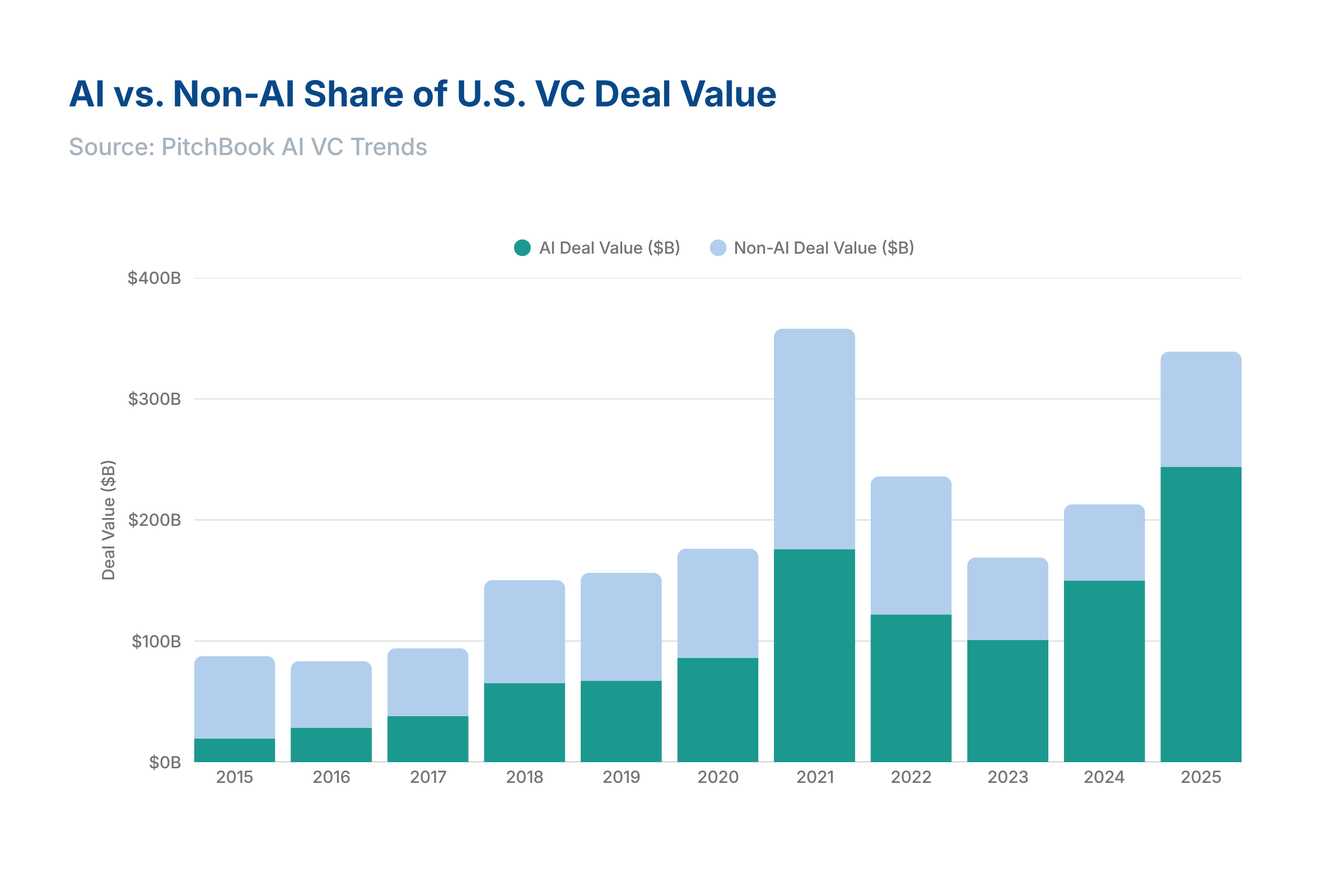

In 2015, AI-related deals represented about 10% of U.S. VC deal value. By 2025, that share reached 65.6%. Two-thirds of venture dollars now flow into a single sector.

AI deal value grew from just under $14 billion to over $222 billion over the past decade, while non-AI venture investment stayed flat at around $117 billion.

For a company in the middle with strong growth but no AI angle, this creates a real fundraising disadvantage. Funds that once wrote $5 million and $15 million cheques are raising larger vehicles. Others did not make it to their next fund. Others started move up even earlier, with a different strategy all-together.

Capital has reorganized around different priorities.

The second force is the legacy of 2021.

Down rounds more than doubled between 2022 and 2023, jumping from 7% to 14% of all deals.

Many businesses caught in this repricing are not distressed. They are growing, often near profitability, and operating in large markets. The problem is timing: they last raised in a pricing regime the current market will not match, so returning to equity now punishes existing shareholders for macro and market shifts rather than business deterioration.

The costs go beyond dilution:

Valuation reset. A down round reduces the price per share and resets the reference point for employees, existing investors, and potential acquirers benchmarking value.

Signalling risk. A down round tells the market that internal expectations missed. For companies performing well, that signal misleads, but investors read it anyway.

Unnecessary dilution. Accepting equity at a compressed valuation means giving up more ownership than fundamentals warrant to fund a plan that might need only 12-18 months of additional runway.

For companies in this band, equity can be mispriced today. The terms can be punitive relative to the underlying business, even when equity is available.

While the first two forces explain why the middle is being squeezed in equity, the third suggests why part of the market may need less equity than before.

The Bessemer State of AI 2025 describes AI ‘Supernovas’ generating $1.13 million in revenue per full-time employee, four to five times a typical SaaS benchmark. AI tools let founders automate and ship with far smaller teams, reducing the need for the headcount that traditional venture rounds were designed to fund.

Forbes suggests that efficiency gain has popularized seed-strapping: founders raise one modest seed round, then scale on revenue, bypassing follow-on VC rounds and keeping more control and equity. The dilution math flips. A $50 million exit barely moves the needle for a company that sold 70% of itself across four rounds. The same exit can return 10x for a founder who kept most of their stake.

Seed-strapping does not prove the broader market needs less equity capital, but it does reinforce the case that a growing subset of the early-stage pipeline can reach meaningful revenue on a single round, reducing future demand for traditional Series A and B funding.

Some of the same dynamics visible in equity appear in debt. But the picture for borrowers is more nuanced, and in several ways more favourable.

Venture debt reached a record $62.4 billion in 2025, surpassing the previous record of $61.1 billion set in 2024. AI infrastructure spending drove the headline growth, but the reshaping of the lending market after Silicon Valley Bank's collapse in 2023 matters more for the middle market. More and more non-bank lenders entered the space. Check sizes grew, structures loosened, and more companies can access venture debt today than at any point in the past five years.

The rapid expansion of private credit reflects a broader shift from bank financing to non-bank lending, bringing more capital, more participants, and more competitive terms to the market. For companies in the missing middle, this creates a window. Lenders are competing for quality borrowers, and well-run companies with strong fundamentals have leverage they did not have two years ago.

Equity today, for this segment, often means accepting a valuation reset disconnected from the business's trajectory. Founders give up ownership not because the company needs more capital than debt could provide, but because the equity market's pricing is misaligned with their fundamentals. A down or flat round that investors read as weakness, regardless of performance.

Debt offers something different. It gives companies time to grow into their valuation and hit the milestones that justify a stronger equity raise. It preserves ownership when dilution is most punitive, and it lets founders choose when to return to the equity market rather than being forced back on the market's terms.

The question is which capital partner to choose: one whose underwriting discipline and long-term approach will serve the company through the full cycle, not at origination alone. In a market with this much capital chasing a shrinking number of quality borrowers, that choice shapes the outcome.

More capital and more lenders mean a wider range of behaviours. Direct-lending spreads compressed in 2025, and deployment pressure stayed high; conditions that can encourage more aggressive pricing and weaker non-price terms.

In practice, that pressure produces two distinct types of lenders:

Deployment-driven lenders need to put capital to work within fixed fund timelines. Their structures tend to look attractive upfront: fast closes, aggressive pricing. They may be less resilient if conditions change.

Discipline-driven lenders, like Flow Capital, are selective by design. They underwrite to fundamentals, structure deals with protections that work in both directions, and preserve the ability to say no. Terms may look less aggressive on paper, but the relationship tends to be more durable through a cycle.

The difference between the two shows up when the cycle turns, not when the loan closes. A well-structured facility extends runway, preserves optionality, and protects the company through volatility. A poorly structured one can create problems worse than the ones it was meant to solve.

Three questions, in order: does debt fit our cash flows? Which lender will support the business through a full cycle? And which structure leaves the company with real flexibility if the next round takes longer than planned?

Near-record capital is in the market, but access is far narrower than the topline suggests.

The debt market has responded. More lenders, increasingly flexible structures, and competitive terms give well-run companies options they did not have two years ago. For founders whose core problem is timing rather than fundamentals, debt preserves ownership, avoids a punitive repricing, and buys the runway to raise equity later stronger terms.

Capital structure is now the strategic decision. In a world driven by capital efficiency, the quality of the capital partner on the other side of the table is paramount.

In a market this bifurcated, choosing the right instrument and the right lender is as consequential as the decision to raise at all.