Growth-stage companies face a financing question that has only become more nuanced over the past several years: should you raise equity, take on debt, or combine the two?

What has changed since this question was first asked is the market around it:

Venture debt has grown from a niche product into a meaningful part of the capital stack. The U.S. venture debt market reached an estimated $53.3 billion in deal volume in 2024, nearly double the prior year, according to PitchBook.

Meanwhile, late-stage tech valuations remain roughly 40% below their 2021 peaks, making equity more expensive in dilution terms than it was during the last boom.

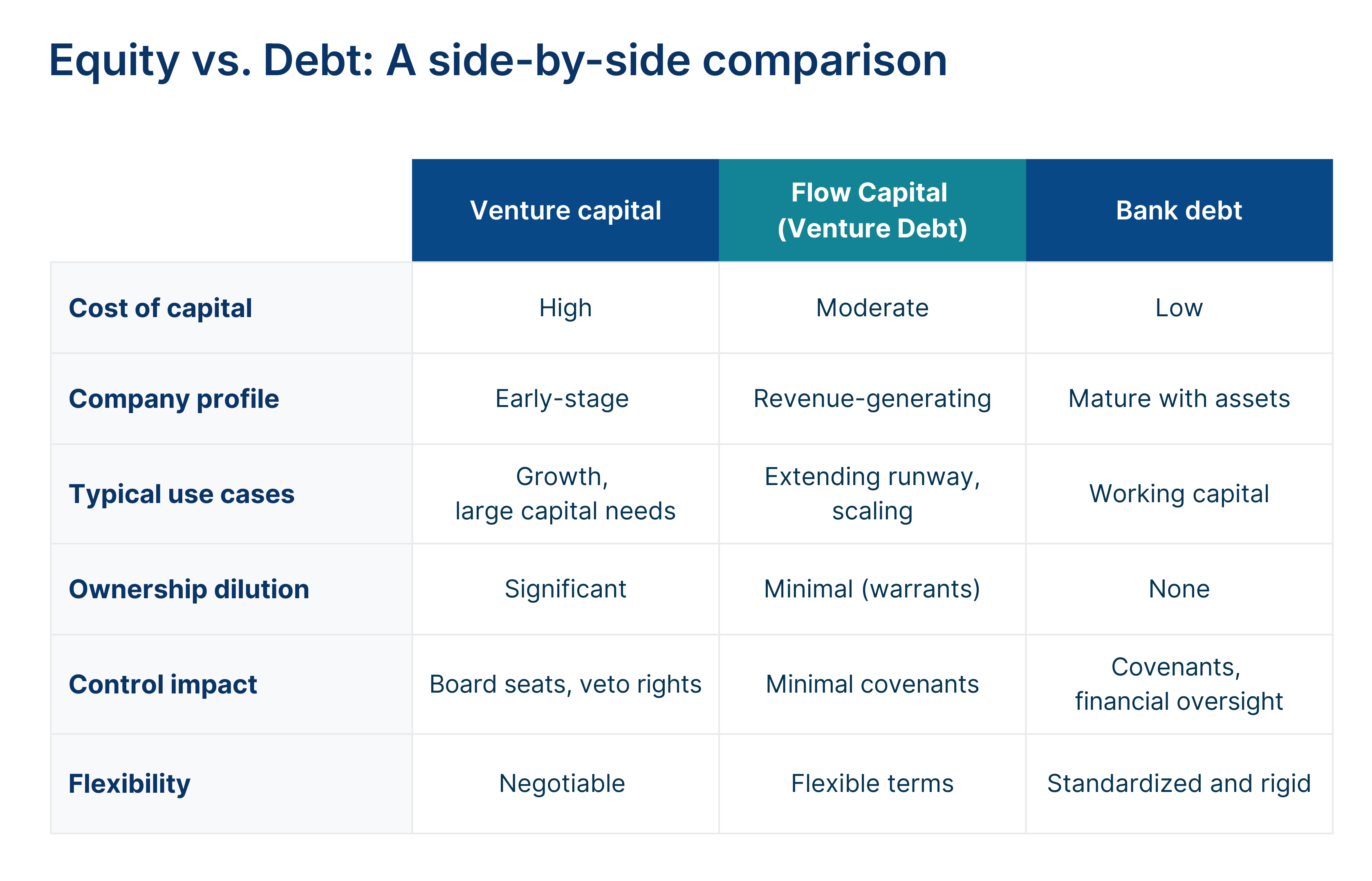

Equity financing involves raising capital by selling a percentage of ownership in your company. Investors, typically venture capital firms, growth equity funds, or angel investors, provide capital in exchange for shares. Their returns come from a future liquidity event: an acquisition, IPO, or secondary sale.

For growth-stage companies, equity investors typically look for established markets, proven unit economics, and a repeatable customer acquisition process where lifetime value exceeds the cost of acquisition. The company may or may not be profitable, but it should demonstrate a credible path to profitable growth.

According to Carta's State of Private Markets data, median dilution in 2025 sits at approximately 19.5% for seed rounds and 18% for Series A rounds. Series A investors generally look for 1530% ownership. These figures are actually higher than the peak of 2021, reflecting a market where capital has become more expensive and investors are demanding more ownership for the risk they take on.

After stacking dilution from a seed round, a Series A, and an employee option pool, founders (along with early angels and pre-seed investors) typically hold around 50% of the company post-Series A. By Series C, that number can drop considerably further.

Debt financing involves borrowing capital that the company repays over time, typically with interest. The lender does not take an ownership stake. Instead, they earn a return through interest payments and, in some cases, modest warrant coverage.

For growth-stage companies, debt financing can take several forms: traditional bank loans, venture debt, or revenue-based financing. Each has different requirements, structures, and trade-offs.

Venture debt has moved from the margins to the mainstream. The global venture debt market reached roughly $49 billion in 2025, and Deloitte projects the asset class could grow to represent 20% of total venture funding by 2027. The collapse of Silicon Valley Bank in 2023 initially disrupted the market, but it also opened the door for specialized private lenders and alternative debt providers to fill the gap.

Venture debt is a form of term debt designed specifically for growth-stage companies. It is typically structured as a senior secured loan with interest-only payments and a small tranche of warrants. Unlike traditional bank lending, it does not require hard assets as collateral, personal guarantees, or the strict covenant packages that banks impose.

Venture debt works best in specific situations. It is not a replacement for equity, and it is not a lifeline for struggling companies. It is a tool for healthy, growing businesses that want to optimize their capital structure.

The math in practice: A company raising $12 million for growth might take $10 million in equity at a $50 million valuation (giving up 20%) and layer in $2 million of venture debt. The alternative, raising the full $12 million in equity, would cost an additional 4% dilution. Over time, that 4% can represent millions of dollars in founder value.

Venture debt lenders have become more selective, particularly since 2023. In today's market, lenders generally look for revenue of at least $2-3 million (often more), a clear use of funds tied to growth, a credible path to the next milestone (whether that is profitability, a follow-on round, or an exit), and a management team that communicates clearly and manages cash thoughtfully. Pre-revenue companies or those treating debt as a last resort are typically not good candidates.

Learn more: 6 Growth Metrics Investors Care About Most

The right financing structure depends on where your company sits today and where it needs to be in 12–24 months. Here are the key questions to work through:

The blended approach: Smart CFOs do not think in terms of "debt or equity." They think in terms of blended cost of capital. Even when equity is available, the all-in cost of debt is often dramatically lower, particularly for companies with strong revenue growth. The most capital-efficient growth-stage companies use both strategically.

1. What is the difference between equity financing and debt financing?

Equity financing involves selling ownership shares in your company in exchange for capital. Debt financing involves borrowing capital that you repay over time with interest, without giving up ownership. Equity is more expensive long-term but has no repayment obligation. Debt preserves ownership but requires cash flow to service payments.

2.What is venture debt, and how is it different from a bank loan?

Venture debt is a form of term debt designed for growth-stage companies. Unlike bank loans, venture debt typically does not require hard asset collateral, personal guarantees, or the strict covenant packages that banks impose. It is structured to work with the cash flow profiles of high-growth companies that may not yet be profitable.

3. How much equity dilution should I expect in a funding round?

In 2025, median dilution is approximately 19.5% for seed rounds and 18% for Series A rounds, according to Carta. By the time a company has raised through Series A with an option pool, founders and early stakeholders typically retain around 50% ownership. Dilution compounds with each subsequent round. For a deeper look, see our Founder's Guide to Equity Dilution.

4. When is venture debt the right choice?

Venture debt is typically a good fit when a company has proven revenue, a clear growth plan, and the ability to service interest payments. It is especially useful for extending runway between equity rounds, bridging to a profitability milestone, or reducing the amount of equity needed in a financing.

See Is Venture Debt a Smart Move for Your Company? for a more detailed assessment.

5. Can I raise venture debt without being VC-backed?

Yes. While many venture debt providers require VC backing, some lenders, including Flow Capital, provide venture debt to both VC-backed and non-VC-backed companies. The key criteria are revenue traction, growth potential, and a sound business model.