Growth-stage operators have spent the past years wiring AI into how they build and how they sell. Faster shipping, swift and nimble teams, tighter feedback loops. The catch is that their competitors, and in some cases their own customers, adopted the same tools.

Companies run better than they have in a decade, but sell slower than they have in years.

Both sides of that trade now show up in diligence: The efficiency shows up in burn, the friction shows up in pipeline, and underwriting has started probing each one.

What now?

Among the founders and operators Flow Capital works with, internal AI adoption has moved past experimentation. Teams that had never used AI beyond ChatGPT reviewing an email, now have over half their employees running five or more agents in parallel. Engineering kicked this off, go-to-market followed, and now finance is close behind. Still, none of these companies plan to cut their workforce. It was about getting more out of the best.

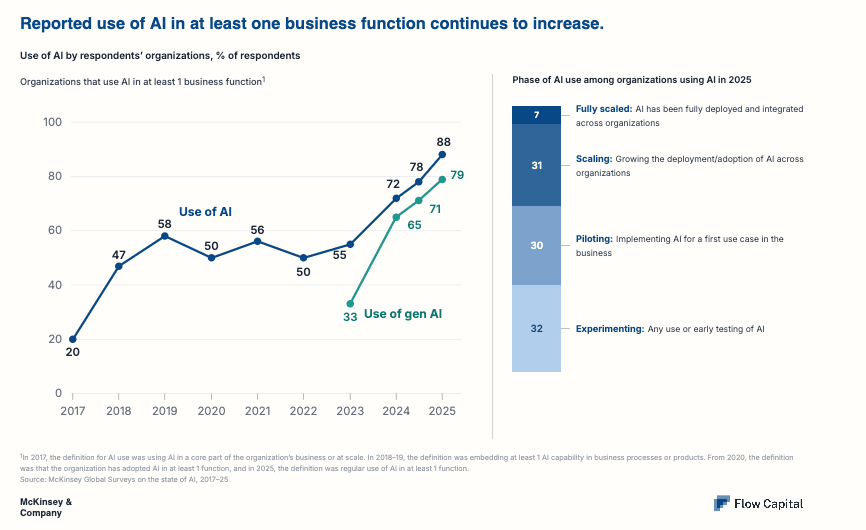

Adoption on its own doesn't tell you who profits from it. McKinsey’s latest State of AI survey draws that line:

The dividing line in that data is workflow redesign. Companies that bolt a tool onto an old process get activity, but there is a lot of noise. Companies that rebuild the process around an elevation tool get results. The high performers also concentrate their bets: a third of them put more than 20% of their digital budget into AI, against 7% of the rest.

The second pattern is a shift in spend. In Flow Capital's conversations with operators, one theme came through clearly: AI is allowing teams to cover more ground without meaningfully increasing budgets. Productivity is rising, while budgets are largely holding.

What is emerging is less about across-the-board cost reduction and more about reallocation. AI is changing where growth-stage companies invest, more than overall spend. For capital providers, that means growth plans increasingly need to be evaluated not just through revenue and burn, but through how AI is changing the pace, composition, and efficiency of that burn.

Sales cycles have lengthened. The average B2B tech sales cycle has stretched now to over six months, from under five in 2019. Some of that shift reflects larger customers adopting technologies they had previously delayed. But the bigger change is a more complex buying enviroment: buying committees have expanded, CFOs are closer to purchasing decisions, and budgets are more transparent across the organization.

Growth-stage companies are selling into a market where demand may still exist, but conversion takes more time, more proof, and more internal consensus. A deal reaches the final stage, and a director asks what happens if a major LLM ships the same capability next quarter. Multiply that pause across a pipeline, and revenue can slip by a quarter without a single obvious lost deal. The demand is still there, but the path to approval has more gates.

Budgets face line-by-line scrutiny. Software has grown from 13% to 21% of corporate tech budgets in five years, and close to half of organizations absorbed renewal increases above 10% last year, with AI features carrying much of the price tag. Finance teams now open renewals with two questions: do we use this, and could a subscription we pay for cover most of it?

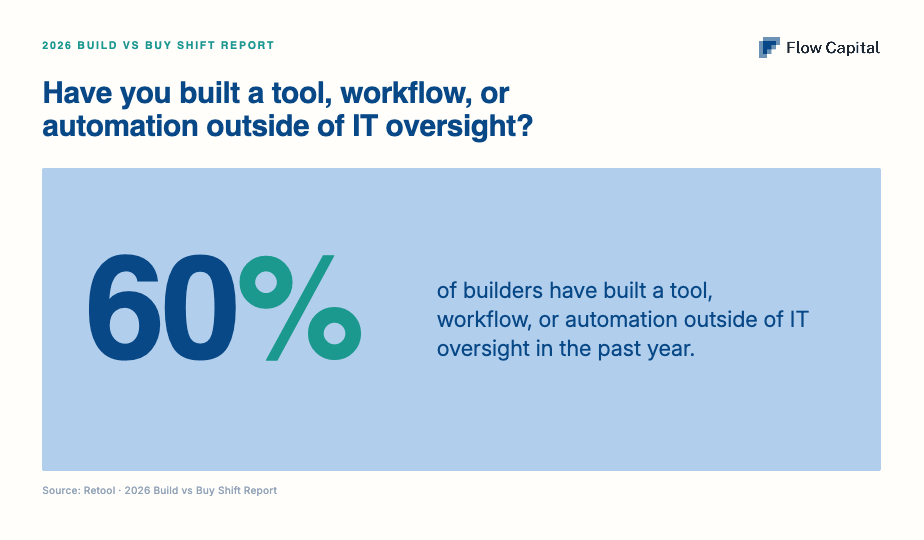

Replacement risk has turned structural. Retool surveyed 800-plus enterprise builders late last year: 35% had replaced at least one purchased tool with software built in-house, and 78% plan to build more in 2026. Gartner expects AI agents to displace about a third of point-product tools by 2030.

The risk is uneven, though. Building still looks cheaper than it is. Code needs maintenance long after the demo, and buyers who experiment with internal tools quickly learn the difference between generating an app and operating one. A vendor who lives inside the customer's problem still wins the contract; products a motivated customer could rebuild in a sprint are far more exposed.

If shared efficiency is not a moat and a model behind a login is not a product, the question becomes: what holds?

Enduring products are more than workflows or LLMs hidden behind a sleek interface. They produce outputs that users depend on to do their jobs. They carry configurations, permissions, compliance requirements, and operational context that are woven into the customer's daily environment.

While there are many nuances between the two, one is easy to spot: does the customer treats the product as a dashboard or as a system? A dashboard summarizes work that happens elsewhere, and a buyer can replace a summary. A system carries the work itself. It is harder, more expensive, and more disruptive to remove.

That distinction matters even more in an AI-enabled product. A product that sits in the flow of customer records accumulates context, and context is what AI can turn into real intelligence. The more embedded the product is, the higher the replacement cost.

Cost structure tells a story as well. Products built on foundation models are riding on pricing that may not stay where it is. What looks viable at today's token prices could look different in 12 to 24 months. Founders should be able to explain where AI costs sit in the P&L and what happens to gross margin if pricing changes. A product that can survive a provider repricing, or a provider outage, is a different underwriting risk than one that cannot.

The same distinction now matters in due diligence. Production-grade revenue, embedded in a core workflow with governance and a real budget owner behind it, can survive procurement cycles and leadership changes. Innovation-budget revenue, funded by a discretionary line or experimental mandate, is more vulnerable in the next round of cuts.

For capital providers, Flow Capital included, the diligence questions are concrete: What in the product is proprietary? Who controls the flow of data? What would a customer lose, in money, time, and risk, by ripping the product out? Could that customer build it themselves?

The answers, however, vary by segment. For example: an SMB customer that ran on spreadsheets two years ago may be able to rebuild a simple tool over a quarter. An enterprise customer paying six figures may already have an internal AI team scoping the same problem. In both cases, the lender is testing the same thing: how deeply the product is embedded, and how expensive it would be to replace.

Retention used to settle much of the product-market-fit question on its own. Gross retention around 90% and net revenue retention above 110% still matter. But now they invite a follow-up: how durable are those numbers?

The criteria themselves have not moved. Retention, GTM discipline, and unit economics determined who could access the right capital in 2020, and they still matter in 2026. What has changed is how hard capital providers stress-test each one before the term sheet.

For founders, that means the best preparation is not just a polished deck. It is a working session on the questions that now shape diligence: where AI sits in the cost structure, what customers would lose by leaving, and which parts of the product a foundation-model release could absorb. Flow Capital is glad to join that conversation early, even when the honest answer is that debt is not the right fit yet.